We wanted to know if regulation of the Buy Now Pay Later (BNPL) industry in the UK would deter consumers, so we surveyed 1,000 BNPL users to find out.

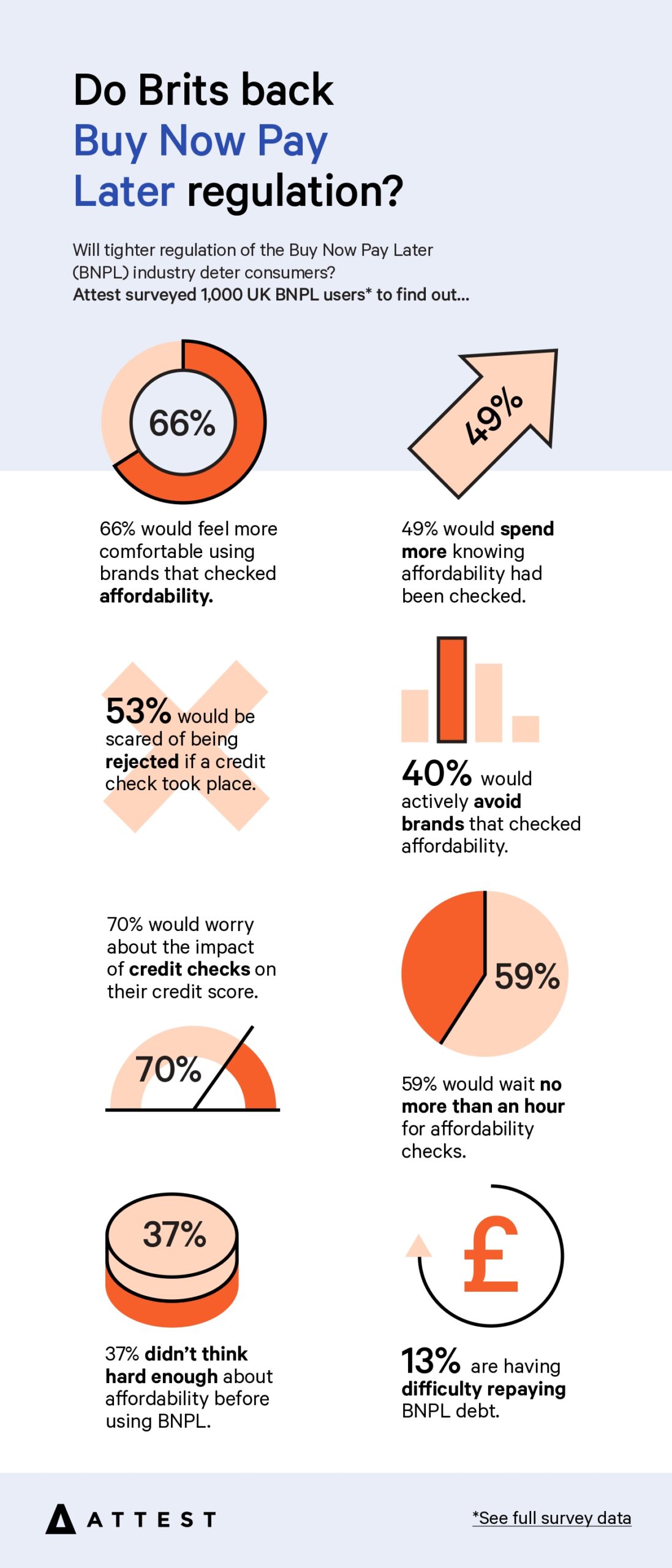

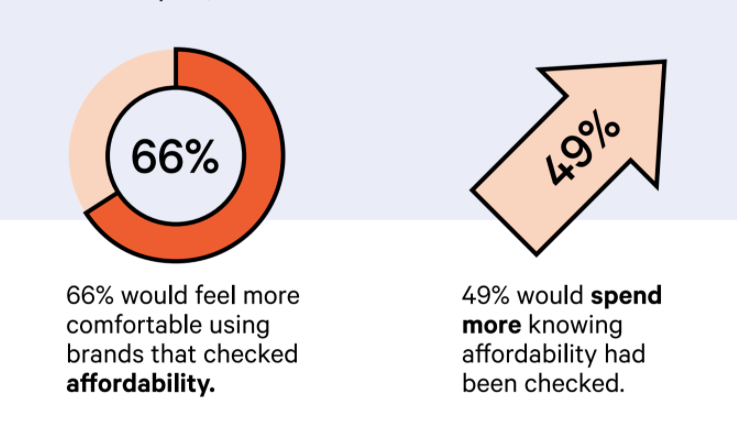

Far from putting people off, the Attest study reveals that almost 49% of consumers would spend more using BNPL knowing that credit checks had taken place and with more transparency as to affordability.

Beyond spend intent, two thirds of customers would feel more comfortable using a provider that verified affordability before purchase, suggesting trust may become the next battleground for BNPL companies. Amongst students, the importance of this affordability check increases, with three quarters of them comforted by this process.

Protection for the consumer if something goes wrong has also emerged as an important driver of choice when selecting a specific provider of BNPL services, ranking fourth behind ease of use, pricing and availability.

“Although stricter controls initiated by regulators at first appeared to be a big blow to the BNPL industry, our research reveals they will in fact build trust and bring the burgeoning payment format into the mainstream,” says Jeremy King, CEO of Attest. “This is good news for all players in this highly competitive space.

Klarna is BNPL market leader

Currently, Klarna, Clearpay and PayPal Credit lead the industry by far in terms of market penetration, used by 63%, 46%, 39% of respondents respectively. Laybuy and OpenPay come in next at 10% each (check out our research on US consumer credit brands here).

The research highlights that BNPL providers need to overcome concerns around credit score impacts and time taken to check affordability, or risk losing customers.

70% of BNPL users worry that by allowing access to personal information for affordability checks to take place, their credit rating could be negatively impacted. 48% say they feel uncomfortable with the idea of their personal information being accessed by a third party. This suggests that clear communications around the process are integral to onboarding customers.

What’s more, as extra roadblocks are introduced for customers using BNPL, speed is going to be vital for discouraging drop off. When asked what the maximum acceptable wait time would be before making a first purchase, 59% stated no more than an hour and 37% said between two and 24 hours.

BNPL users don’t want to wait

Zilch money is currently the only fully regulated provider in the UK, and their website states that credit checks and verifications can take up to 72 hours. Attest data suggests only 10% would be happy with this delay.

The desired transparency of the process and the speed of completion shows the urgency for credit agencies and BNPL providers to begin working together and building infrastructures to deliver on this, ensuring onboarding processes are quick and smooth.

Jeremy King continues, “If transparency and speed can all be achieved, BNPL can become an even more accessible, safe and economical longer term alternative for customers beyond credit cards and personal loans. As regulation and consumer expectations evolve so quickly, BNPL providers need to listen to their audiences at this time, to make sure that any changes imposed off the back of the new regulations are genuinely favourable to the end consumer.

“As we can see in the data, this new regulation can be highly liberating for consumers while also building-in important new control and transparency, and that’s an exciting opportunity for BNPL leaders and attackers to be bigger and better businesses.”

BNPL feels like “free money”

Attest conducted this research in light of the recent Woolard Review from the Financial Conduct Authority, which concluded there was “significant potential for consumer harm” from the largely unregulated BNPL industry. The controversy surrounding the industry gained a spotlight earlier this year as concerns grew over the rise of BNPL during the pandemic, with consumers spending more than they can afford. These concerns are mirrored in the results of the Attest study.

35% stated that the service was so easy to access that they “didn’t think hard about affordability”, and 20% stated it felt like “free money”, rising to 23% amongst 18-24 year olds.

As a result, 17% of those surveyed said that their debt had crept up without them noticing, 17% had their credit score impacted and 13% are having difficulty repaying. Not surprisingly, younger age groups have been hit harder, with one in five BNPL users amongst Gen Z (18-24) consumers stating that their credit score has been impacted, and 17% struggling to meet repayments. Even more worryingly, 13% are having to borrow more money to pay off their BNPL debts.

Of course, the introduction of more robust credit checks is going to result in some users being blocked from using BNPL services. 53% expressed concern that they would be rejected for BNPL services if their affordability was checked.

The results from this original research can be viewed on Attest’s interactive dashboard.

BNPL infographic