US direct-to-consumer report 2022

As inflation bites, what’s the outlook for direct-to-consumer shopping in the US? In this report, we take data from 2,000 working-age Americans to help brands understand how consumer behavior is changing in response to the cost of living crisis – and what they should do about it.

The findings at a glance

Chapter 1

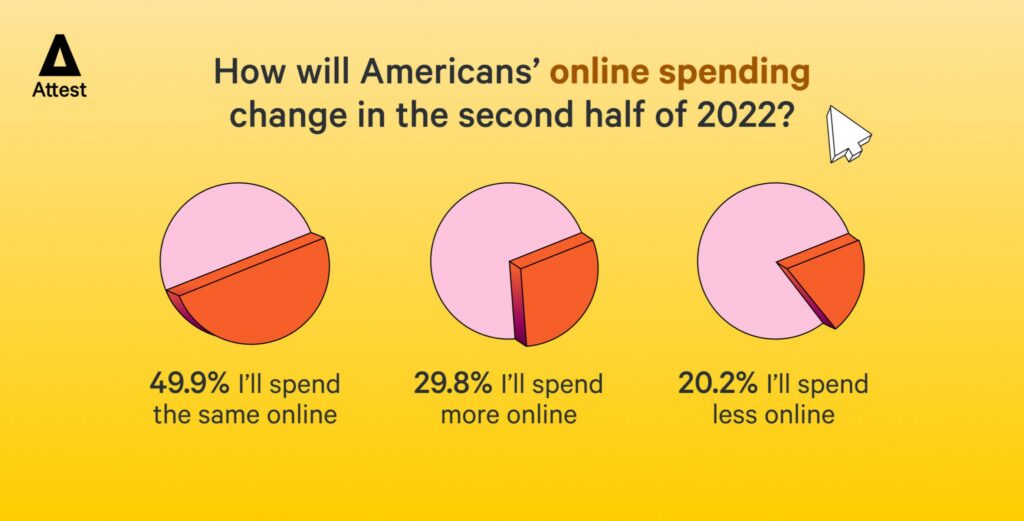

The current economic downturn means challenging times are ahead for many Americans. Encouragingly, though, the growth seen by many online retailers during the pandemic could be set to continue in spite of the cost of living crisis. Even in the face of rising inflation rates, our direct-to-consumer (D2C) shopping survey of 2,000 working-age, nationally representative consumers shows Americans expect their online spending to go up over the next six months.

Just over 20% of people think the amount they spend will decrease, while 29.8% think it will increase, resulting in a net 9.6% of people who will be spending more online. However, we should temper our optimism; this data probably doesn’t indicate a spending spree. More likely, people think they’ll favor online shopping over in-store as a way to find better deals, or they’re anticipating having to spend more simply because of the rising cost of products.

Even for the 49.9% of people who say their spending will stay the same, their reduced spending power could lead to them being able to afford fewer purchases. But it’s still interesting to note that the biggest increase in spend will be seen among those aged 35-44 (who happen to be the most frequent online shoppers), and those aged 25-34. A net 13% of 35-44 year olds and 12.9% of 25-34 year olds predict a rise in expenditure in the coming months.

How much do people spend online currently?

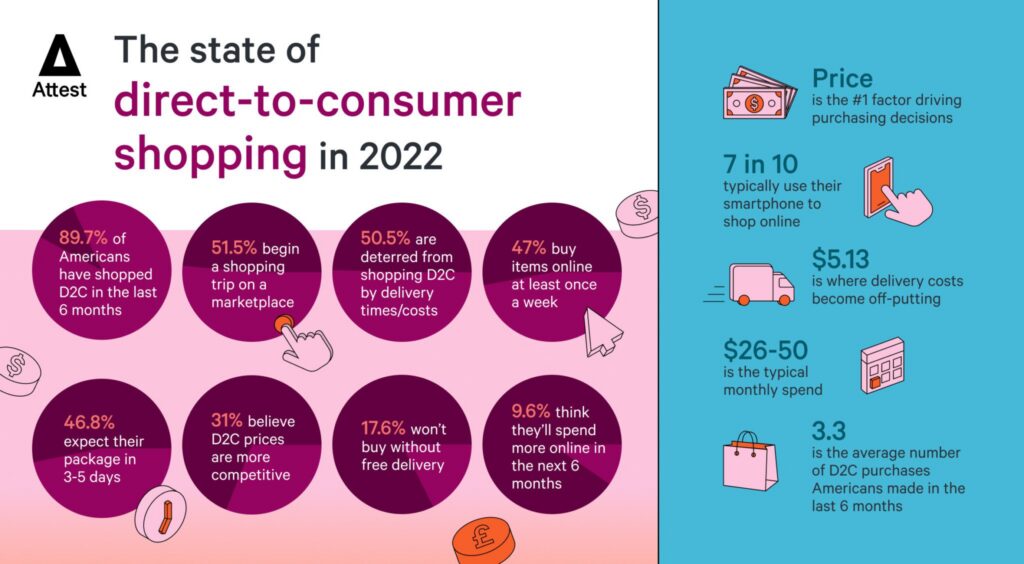

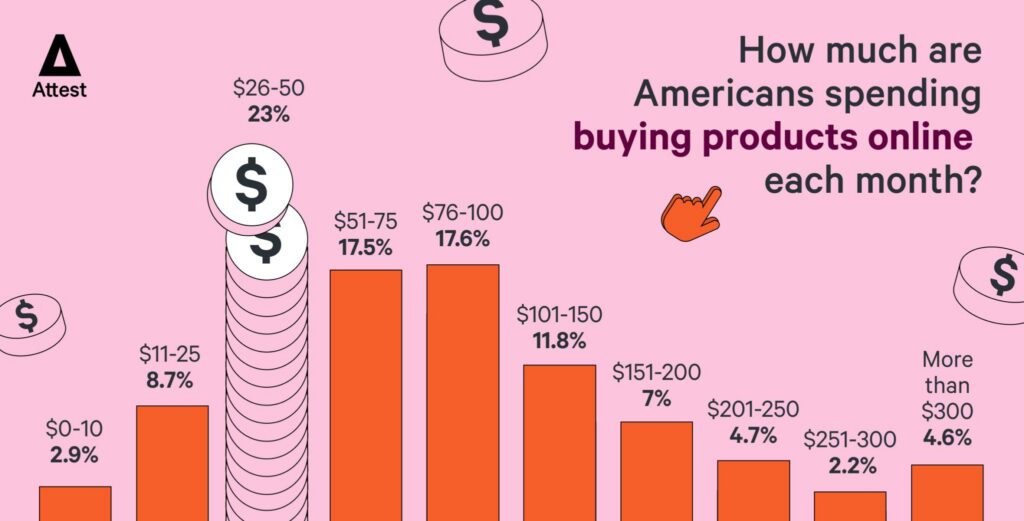

To understand what that increase might look like in monetary terms, let’s look at how much people are spending online at the moment. The single largest percentage of people (23%) spend between $26-50 per month, while 11.6% spend less than this. The remaining 65.4% spend in excess of $50 buying goods online each month, with 30.3% spending more than $100.

Notably, it’s these highest spenders who are most likely to say they’ll be spending more in the next six months; a net 18.6% of people who spend $100+ say they’ll increase what they spend. In comparison, among those who spend between $11-25 per month, a net 0.6% say they will actually reduce spending in the next six months. We can conclude, then, that retailers selling smaller ticket items are likely to feel the impact of the cost of living crisis more than retailers of higher value items.

Currently, Americans are shopping online with high regularity; 47% buy items online at least once a week, while a further 8.1% shop fortnightly. People aged 25-34 are the most frequent online shoppers; 27.4% shop more than once a week, followed by 23.6% of 35-44 year olds.

Which categories are most at risk?

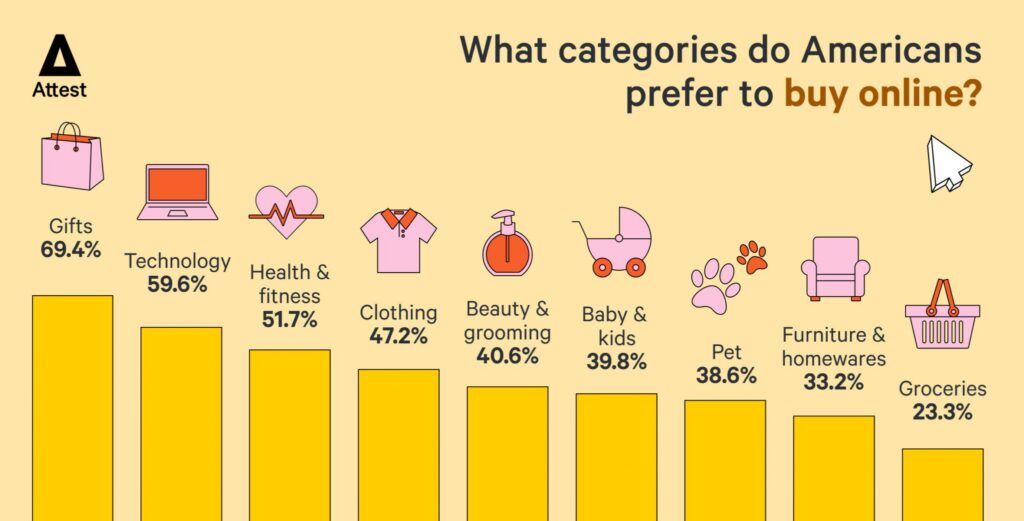

Now the dust is settling on the pandemic, we wanted to know which categories people are most likely to be shopping for online and which they prefer to buy in a store. There are some notable categories that Americans show a strong commitment to buying online; these are gifts (69.4%) and technology (59.6%).

However, there are a great many things that Americans clearly prefer to buy in store. Among these are groceries (76.6%), furniture & homewares (64.6%), beauty & grooming products (58.1%) and pet products (53.1%).

Then there are the categories where people are equally likely to shop in both channels: health & fitness, baby & kids, and clothing. Retailers in these “up for grabs” categories will have to work harder to capture customers and should focus on communicating how shopping direct can be cheaper than at bricks-and-mortar stores. As we’re about to find out, value-related messaging will be all-important in the second half of 2022…

Chapter 2

With inflation causing the price of many products to rise, it figures that people will be looking for the best possible value. In fact, price will trump all other factors when it comes to winning D2C customers this year. Respondents to our survey ranked price as the most important factor in their purchasing decisions, with quality taking second place. There is a clear distance between price (ranked 2.7) and quality (ranked 3.2), underlining just how price conscious today’s D2C shoppers are.

D2C brands are traditionally perceived to be cheaper than bricks-and-mortar stores, but this belief seems to be in decline; today, 31% of people believe the prices to be more competitive, compared to 35.8% who said the same in November 2020. Online retailers need to ensure they address this changing perception if they want to score an advantage as the cost of living crisis worsens.

But it’s not just about offering the cheapest prices. In a separate piece of research conducted among U.K. shoppers that explored what ‘value for money’ means to D2C customers, we found that most were looking for ‘affordable quality’ (32%). A further 20% want to buy something that will last a long time, while 19% want to feel like they’re getting more than they pay for. This suggests messaging should remain nuanced, expressing great value for money over simply rock bottom prices.

What else do shoppers want?

Behind price and quality, ‘delivery cost’ was ranked as the third-most important factor. We’ll delve further into this factor in Chapter 4, but it’s worth noting at this point that retailers face a real challenge on this front. Shoppers are keenly aware of delivery charges and will factor these costs in when making their assessment of what constitutes good value.

Americans ranked ‘choice’ as the fourth-most important factor when shopping D2C. This might seem like bad news for smaller brands, but you can play to this desire without growing your range. By letting shoppers know that your entire product range is available on your website – as opposed to a limited selection that might be offered by third party retailers – you can give consumers a bigger reason to shop with you directly.

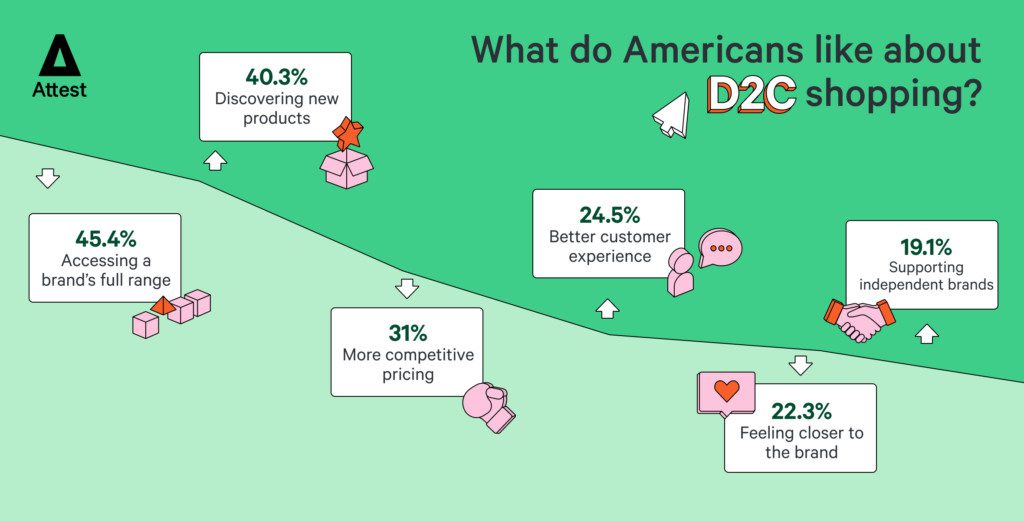

In fact, you might be surprised to learn that the highest perceived benefit of shopping directly with a brand is being able to access their full range (45.4%). This answer has increased in popularity since November 2020, when it was only the second-rated benefit at 41.1%.

Discovery of other products was the second-most popular reason people liked using D2C websites, having been the most popular reason two years ago; 40.3% of people say they liked this way of shopping because they end up discovering other products they might like. People aged 18-24 over-index for liking D2C shopping for this very reason (47.9%). But consumers in this age range also believe D2C shopping lets them feel closer to the brand (21.3%) – information that brands should absolutely capitalize on when devising marketing strategy for this age group.

What factors should take a back seat?

In leaner times, it can also be helpful to know what’s less important to consumers so you can focus your resources where it counts. When we asked people to rank the factors that influence their decision to buy from a brand’s website, they were least likely to say ‘ease/cost of returns’, ranking it 8/8. Returns policy is the type of thing that becomes a positive or negative factor after purchase, so it’s still important for brand reputation, but it doesn’t need to be a lead message for conversion.

Brand image and brand values are also deemed to be less important when weighed up against more practical considerations like price, quality and delivery. Likewise, only 22.3% of people say they like D2C shopping because it lets them support smaller or independent brands.

With this in mind, it’s clear that brands should put the consumer at the center of their marketing campaigns. How can you help them to save money? How can you help them to care for their nearest and dearest? What extra value can you deliver? These factors become especially important when people have less disposable income.

Chapter 3

To maintain sales in 2022, it’s not just about updating your message to consumers, it’s also about ensuring you deliver it to them in the right places.

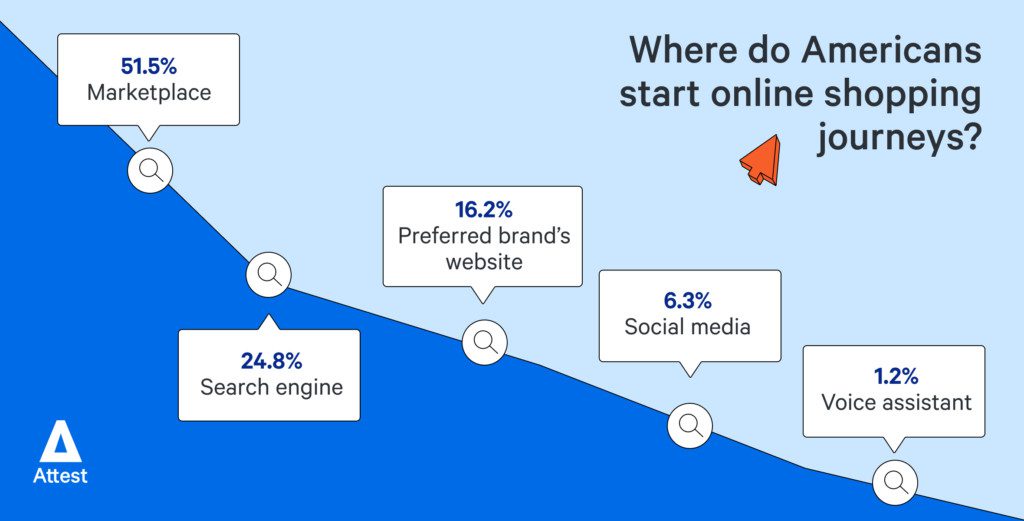

The bad news for D2C retailers is that the majority of Americans (51.5%) start their online shopping journeys on a marketplace such as Amazon, rising to as much as 56% in the 55-64 age category. It means that D2C brands may have no option but to be present on Amazon and relinquish control of their stock to FBA.

But there are some reasons for optimism; search engines rank second, with 24.8% of people typically starting a shopping mission there, climbing to 27.9% among 45-54 year olds. Brands need to set aside a significant portion of their marketing budget for Google AdWords and SEO, then, in order to maximize their chances of tempting shoppers to their website.

The need to invest in search is underlined by the relatively small number of consumers heading directly to a preferred brand’s website when they want to buy something. Only 16.2% of people say they’re most likely to start a shopping journey in this way, dropping to 14.5% among the key 35-44 age group.

How tech savvy are D2C shoppers?

While social media is only a starting point for online shopping journeys among 6.3% of Americans, this figure rises to 10% among 18-24 year olds and 11.4% in the 25-34 year old category. This shows that brands catering to younger consumers can get significant mileage from advertising on social media and enabling in-platform shopping features. At the other end of the scale, social media is a starting point for just 0.8% in the 55-64 range, so brands targeting older consumers should adjust their ad spend accordingly.

On the other hand, what we can say with confidence is that brands don’t yet need to worry about investing in voice search as a priority. Only 1.2% of people typically start a shopping journey using a voice assistant.

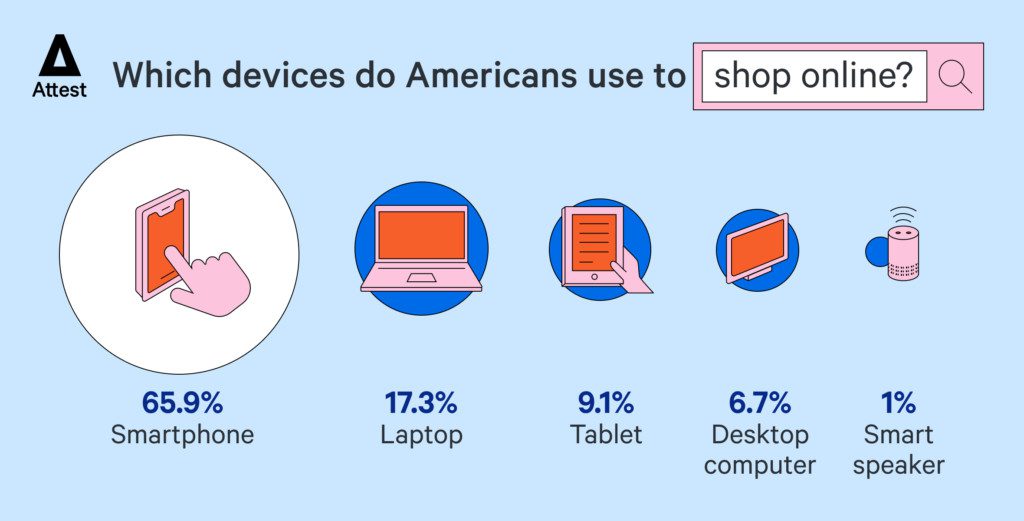

Smartphone shopping, however, is massively popular; 65.9% of Americans say they most frequently use their mobile to research or make purchases online, rising to 79.3% in the 25-34 age range. Optimizing your website for mobile and making the shopping experience as frictionless as possible is therefore a must.

While the smartphone is well ahead of other devices as a shopping tool, it’s worth noting that older shoppers over-index for using desktop computers, laptops and tablets for visiting D2C sites. This highlights the need to ensure your website has the necessary accessibility features enabled in order to support shoppers who might find using a smartphone tricky.

What keeps people coming back to D2C?

While starting a shopping mission on a brand’s website isn’t that common, actually buying from D2C retailers is a very frequent occurrence. Some 85.6% of Americans have shopped D2C in the last 6 months, and they’ve made an average of 3.3 purchases.

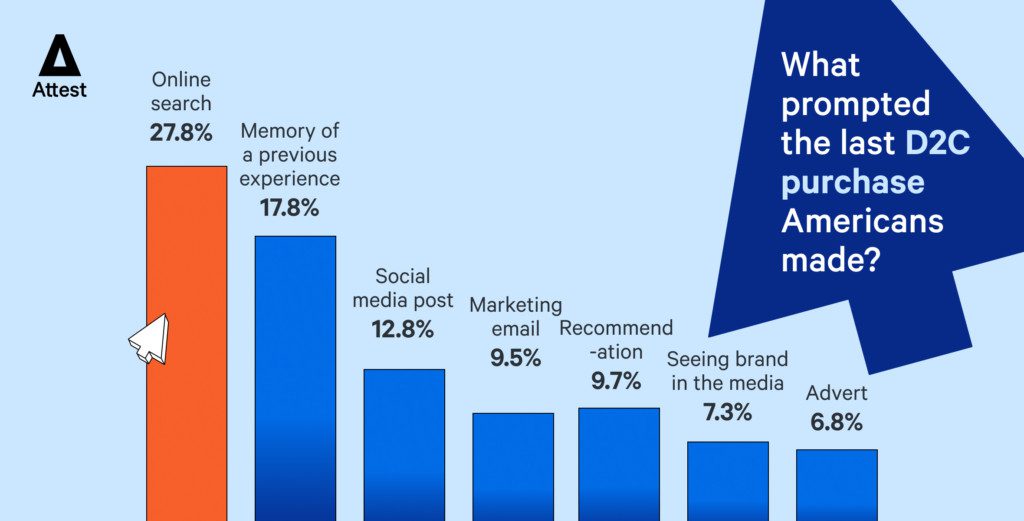

And yet the memory of a good shopping experience with a brand may not always be enough to drive a repeat purchase. While 17.8% of respondents said the memory of a previous experience drove them to make their last D2C purchase, a larger 27.8% said it was driven by an online search.

Perhaps this means D2C brands are not doing enough to establish loyalty? But, on the plus side, if people head to a search engine when they want to make a purchase, it also means there are more prospective customers for new brands. The important thing is for D2C brands to be visible – especially as word-of-mouth appears to lack its usual power in this sector (just 9.5% of people said their last purchase followed a recommendation from a friend).

The effectiveness of other tactics also pale in comparison to search; 12.8% were driven to make a purchase by a social media post, 9.5% by a marketing email, 7.3% by seeing the brand featured in the media, and 6.8% by an advert. There were a few differences in drivers between the demographics that are worth pointing out. Shopping trips by those aged 18-24 were especially likely to be prompted by social media posts (22.8%) and media features (9.5%). Meanwhile, recommendations were most important for those aged 25-34 (11.5%).

Chapter 4

Delivery times and costs are a key battleground for D2C sellers, with everyone competing to do it faster and cheaper. Delivery cost is especially important. Our data shows that delivery cost is the third-most important factor that drives Americans to purchase, behind price and quality.

We also see that poor delivery terms act as a major deterrent to online shoppers. More than half of people say long delivery times/high delivery costs deter them from buying D2C, which is a massive jump from November 2020 when just 35.6% rated this as a concern. In comparison, only 31.7% of people are put off by the inability to try products, and 27.3% by the inconvenience of returning products.

And concerns about data security while shopping online are dwarfed when compared with worries about shipping (though a significant proportion – 20.5% – are deterred by website security concerns). This really puts the importance of good delivery terms into perspective. So what do shoppers expect from D2C brands when it comes to delivery?

How long will shoppers wait for delivery?

Delivery time was ranked as only the sixth-most important factor that drives Americans to make a D2C purchase. It seems that the pandemic helped many consumers recognise the need for patience – we all understand the pressure that COVID put on delivery services, while media images of container ships lining up outside ports nationwide are fresh in the memory.

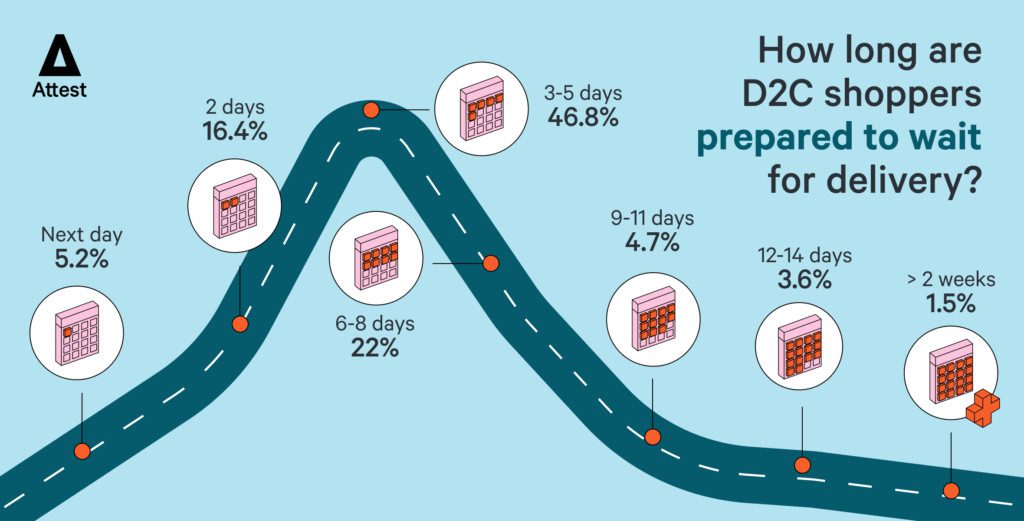

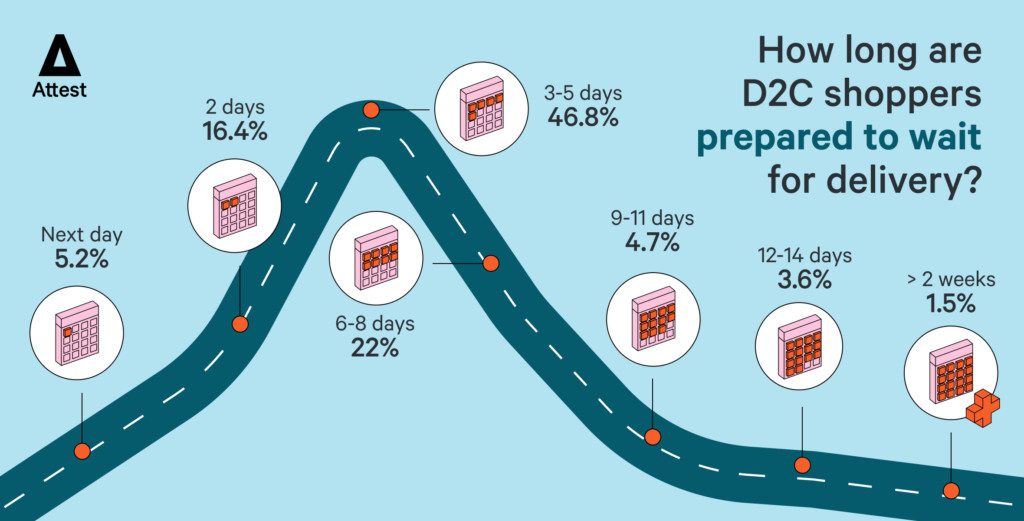

A significant proportion of consumers – 22% – said they’d be happy with delivery in 6-8 days, while 9.7% are prepared to wait 9 days or more. However, brands should note that the majority (46.8%) of Americans expect to receive their package in 3-5 days, so they shouldn’t be complacent about delivery speeds. And there remain those more demanding consumers who want next day delivery (5.2%) and or delivery within two days (16.4%).

Delivery time expectations do vary between demographics though; those aged 18-24 will wait the longest (17% said they would wait in excess of nine days), while those aged 35-44 are the most likely to say they won’t wait longer than two days (27.5%).

What are shoppers prepared to pay for delivery?

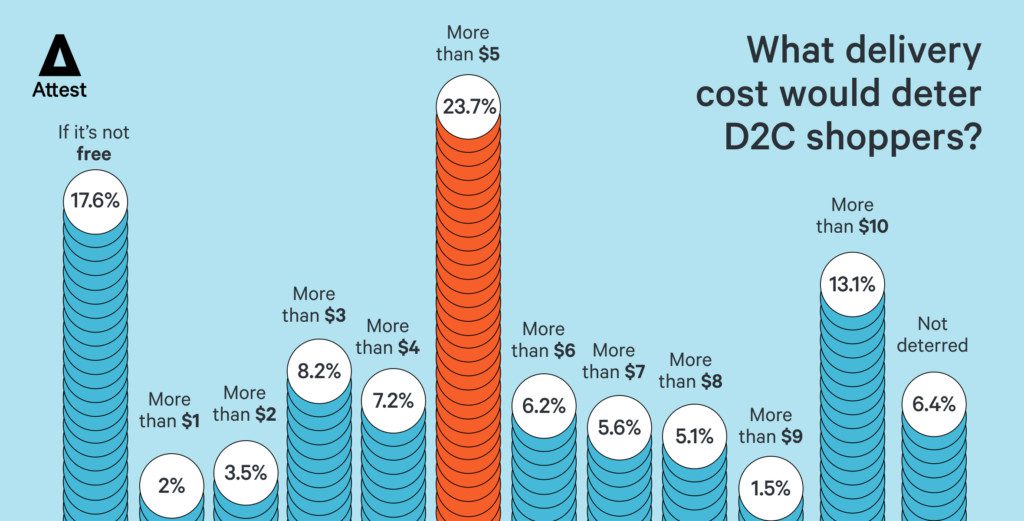

There’s no denying that free delivery is a major plus for consumers, but is it a deal-breaker if D2C brands don’t offer it? The answer is no; only 17.6% of Americans would be deterred from making a purchase if delivery was not free.

But the expectation for free shipping does differ depending on your age, and it‘s not necessarily in the way you would expect. It’s people aged 55-64 who are the most likely to say they’re deterred if delivery is not free (22.1%). Meanwhile those aged 18-24 – often thought to be the most demanding – are the least likely to care about free delivery (12.4%).

The good news is that most people are prepared to pay for delivery of their goods – albeit not huge amounts. The average price point where Americans will start to be deterred from ordering is $5.13. A decisive 79% of people would not pay over $8 for delivery. However, very few people expect to pay less than a buck (2%), meaning that levying a reasonable charge for delivery shouldn’t affect your sales.

In terms of how Americans want to pay for D2C purchases, credit or debit card is still the most popular option with 51.5% of respondents, slightly strengthening from November 2020 when this option was favored by 49.3%. The popularity of PayPal has shrunk to 27.3% from 31.2% two years ago, while – perhaps surprisingly – Apple Pay has grown only very slightly from 5% to 5.6%. Amazon Pay and Google Pay have actually decreased in popularity, so retailers considering updating their websites to support these types of payment may be better off focusing their efforts elsewhere.